The East London Credit Union’s collapse: major new revelations, and the bad odour intensifies UPDATED

As previous posts (referenced below) have pointed out, the collapse into administration on 11 September 2019 of that longstanding LBWF favourite, the East London Credit Union (ELCU), has left many questions unanswered.

Gradually however, new information is trickling out, and some of it, to say the least, is both startling and deeply worrying, particularly about what has been going on in the Town Hall.

The headline revelations are:

LBWF states it gave ELCU £326,152 between 2014 and 2018, but the real figure is likely to be nearer c. £1m..

LBWF cannot produce any documentation authorising and recording its transfers to ELCU, nor can it credibly explain why not.

In the seven years prior to its financial collapse in 2019, and despite the fact that it was carrying out banking functions, ELCU only produced one set of finalised annual accounts, thus contravening not only the relevant legislation, but also its own rulebook.

Cllr. Paul Douglas’ resignation from the ELCU board still has not been reported to the official regulator, the Financial Conduct Authority (FCA), though nearly three years have elapsed since it happened.

The detailed evidence is as follows.

LBWF subsidisation of ELCU

It has always been known that LBWF subsidised ELCU, though the particulars have remained elusive.

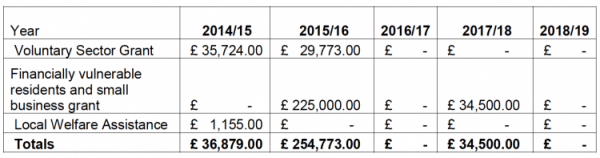

Asked under the Freedom of Information Act (FIA) about this a few weeks ago, LBWF states that ‘the sums per annum’ it paid over to ELCU in the period 2014-19 were as it tabulated here:

That looks definitive, but there is a problem.

Because, in an edited book published in 2017, Austerity, Community Action, and the Future of Citizenship in Europe, two contributors, Paul A. Jones and Michelle Howlin, state: ‘As a sign of growing confidence in the capacity of the credit union to deliver alternative financial services to the population at large, in 2015, the London Borough of Waltham Forest made a £500,000 investment to deliver a range of initiatives, including business lending’.

Of course, Jones and Howlin may have got this wrong, may have simply misunderstood what was going on.

But the fact that Michelle Howlin, aside from co-writing the chapter cited, was CEO of ELCU from 2012 to its collapse rather suggests otherwise.

So why doesn’t the £500,000 ’investment’ show up in LBWF’s figures?

LBWF’s documentation of payments to ELCU

Relatedly, and concentrating only on the payments to ELCU that LBWF does acknowledge making, there are issues about authorisation and recording.

LBWF states that, when paying out money, it either responded to ‘invoices addressed as Waltham Forest community credit union’ (ELCU’s formal name) or ‘paid directly to their vendor account (email payment request)’.

LBWF’s ‘Transparency’ pages list all the invoices over £250 it has settled since 2012.

However, a thorough search finds not a single invoice either from or to the ‘Waltham Forest community credit union’.

Moreover, it does seem a bit strange to hand over large sums of public money solely on the basis of an e-mailed request. Why didn’t LBWF use the invoice system throughout?

But there is more.

For when asked recently, and very specifically, for copies of ‘the invoices and e-mail requests’ that LBWF had referred to, Director of Governance and Law Mark Hynes referenced the table reproduced above, and commented as follows:

(a) re the £295,000 to support ‘Financially vulnerable residents and small business grant’:

‘The Service have reviewed the information they hold and advised that they have identified information that they are able to release to you within the scope of your [previous] request [sic]’.

(b) re the £65,497 ‘Voluntary Sector Grant’: ‘The Council is unable to provide any information…as that team was disbanded a few years ago and any manual records held were securely destroyed’.

(c) re the £1,155 Local Welfare assistance grant: ‘We are also unable to provide the requested information’.

In terms of being an explanation, this is pretty feeble stuff (particularly the reference to ‘manual records’, as if the period at issue is the 1970s).

But, that accepted, it clearly demonstrates, too, that even the formidable Mr. Hynes is unable to disguise some fairly big holes in LBWF’s record keeping.

ELCU’s annual accounts

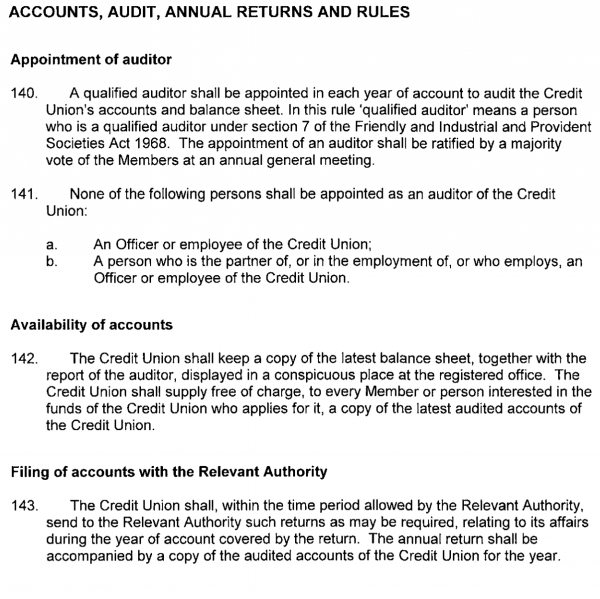

Under the legislation, and like all mutuals, ELCU was required to compile annual accounts, as its rulebook forthrightly states:

Up to 2016, it was also best practice to forward these annual accounts to the FCA, while subsequently such reporting became mandatory.

Up to 2016, it was also best practice to forward these annual accounts to the FCA, while subsequently such reporting became mandatory.

Many no doubt will assume, given this background, that such responsibilities were carried out diligently.

But were they?

Surprisingly, though it was accepting deposits from the less well-off and grants from the public purse, in recent years (at least) ELCU itself appears not to have published anything approximate to annual accounts.

But, surely, public shyness notwithstanding, ELCU must have produced annual accounts?

ELCU’s internal papers have never been in the public domain, thus cannot be used to cast light on its accounting practices.

But ELCU dealt extensively with both LBWF and the FCA – paymaster and regulator respectively – so can they help?

Well, when LBWF was asked under the FIA for copies of ELCU’s annual accounts, it responded: ‘The requested information is already in the public domain and audited accounts can be found in the FCA’s Mutual Public Register [sic]’.

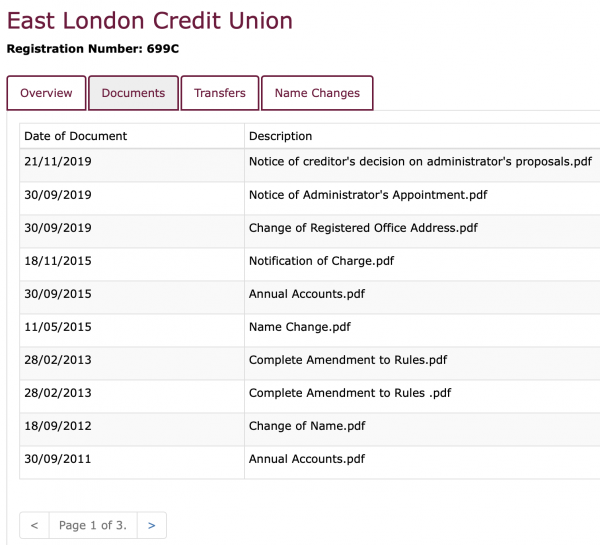

That sounds authoritative, except that, if the FCA’s Mutuals Public Register is consulted, it reveals that while from 2003-04 to 2010-11 ELCU submitted its annual accounts in the normal way, subsequently the situation changed, as this screenshot illustrates:

In summary, during the course of the seven years leading up to its 2019 collapse into administration, ELCU is recorded as having submitted annual accounts just once, in 2014-15.

What does the FCA think about this? Asked specifically about the period after 2016, because that was when, to repeat, reporting was mandatory, the FCA response is curt, though crystal clear: ‘The Credit Union has not submitted its accounts’.

All this is at first sight puzzling, but the explanation turns out to be very straightforward.

For a request dated 20 November 2019 to ELCU’s administrator, Cork Gully LLP, for copies of ELCU’s accounts between 2014 and 2019 elicits the following:

‘The only information in this regard is that registered on the FCA Mutuals Register. Unfortunately, the accounts you refer to were not finalised and I am therefore unable to provide these to you.’

The riddle is solved: from 2010-11 onwards, and with one exception, 2014-15, ELCU somehow got away without compiling finalised annual accounts at all, and neither LBWF nor the FCA apparently raised a finger.

Cllr. Paul Douglas

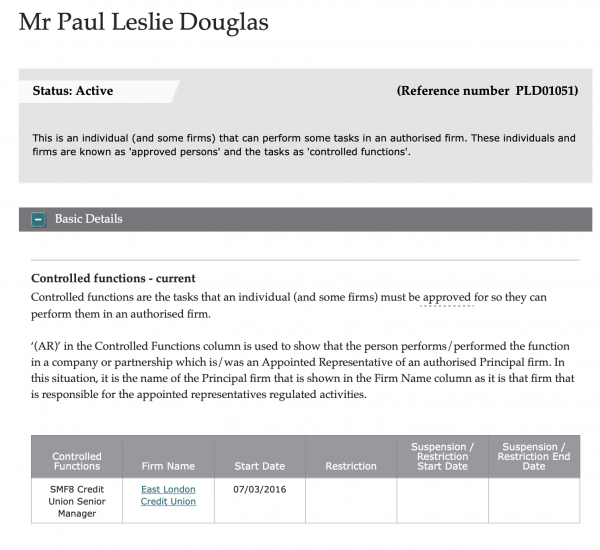

As of today, the FCA lists Cllr. Paul Douglas as an ‘active’ ELCU ‘senior manager’ and board member:

Questioned about this, Mr. Hynes claims that Cllr. Douglas was ‘a Director Of [sic] ELCU up to January 2017’.

The FCA comments:

‘We have checked our records and we approved Mr. Paul Leslie Douglas in 2012 as CF1 (Director function) at ELCU. He was then assigned the SMB8 [Credit Union Senior Manager] function in 2016, as per information on the FSR [Financial Services Register].

We have not received subsequent notifications from ECLU in relation to the above individual.

Part of the FSR contains material sent to us by third parties. These third parties are responsible for ensuring that the material they submit to us is accurate and complies with all applicable legal requirements’.

Taking these statements at face value, therefore, it appears that in the nearly three years that have elapsed since Cllr. Douglas resigned from ELCU’s board, neither he nor ELCU has bothered to tell the FCA, without doubt an unusual way of carrying on, to put it politely.

In conclusion

As the preceding paragraphs demonstrate, ELCU’s corporate affairs appear both unusual, and riven with flaws.

Why was such an unsatisfactory situation allowed to persist?

As has been pointed out before, ELCU was very much a Labour baby – several of its top brass had links to the party, with its President working for Dawn Butler MP, of ‘jacuzzi on expenses’ fame – and given that the political establishment in Waltham Forest has long been Labour, too, perhaps that in part explains why nobody in the Town Hall or elsewhere blew the whistle.

In addition, the FCA’s timidity also has played a part.

Over the last few years, criticism of the FCA has mushroomed, and this case, relatively minor though it is, well illustrates why.

In a nutshell, what’s the point of a regulator that doesn’t actively regulate, and without fear or favour?

ADDENDUM

Since composing this post, a detailed, but possibly significant, matter has come to light.

The FCA Mutuals Register includes a ‘Notification of Charge’ document concerning a debenture that ELCU took out with Nat West.

FCA stamps show that this was received on 25 November 2015, and certified on 14 December 2015.

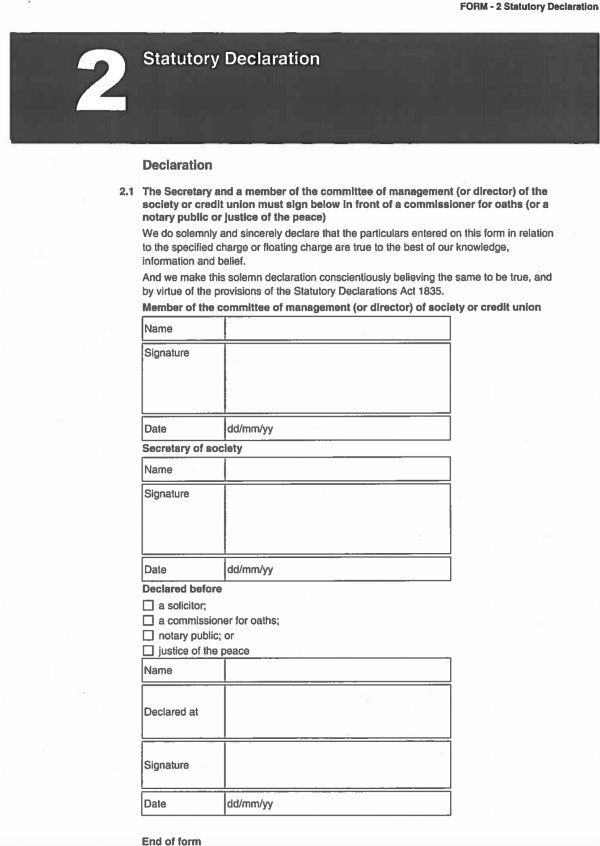

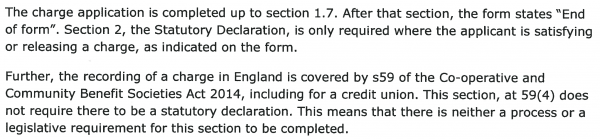

What’s intriguing is that the Statement is incorrectly filled in, with the mandatory section two, ‘Statutory Declaration’, left completely blank:

Why didn’t the FCA pick this up?

UPDATE

Regarding the latter, the FCA comments:

This is interesting, because it confirms that ELCU had not paid off the ‘Charge’, a debenture, at the time it went into administration, suggesting that there will be another substantial call on ELCU’s remaining assets which the administrator will have to sort out.