Cllr. Paul Douglas and the East London Credit Union: confusion reigns

As a previous post pointed out (see link below), the demise of LBWF’s beloved East London Credit Union (ELCU) throws up a number of as yet unanswered questions.

Some recent correspondence adds to the confusion.

On 26 September 2019, I wrote to LBWF’s Director of Governance and Law, Mark Hynes, as follows:

‘Dear. Mr. Hynes,

As of today, Cllr. Paul Douglas’s register of interests form records that he is ‘a member’ of the East London Credit Union…

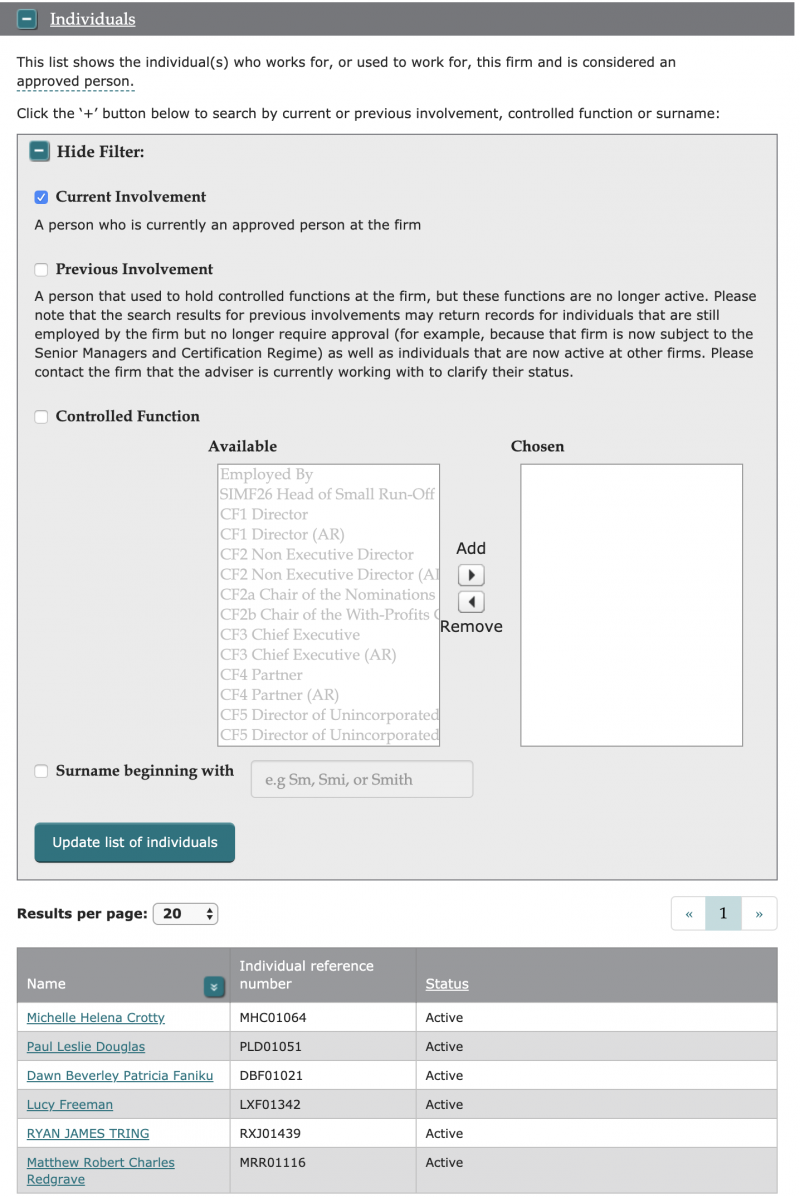

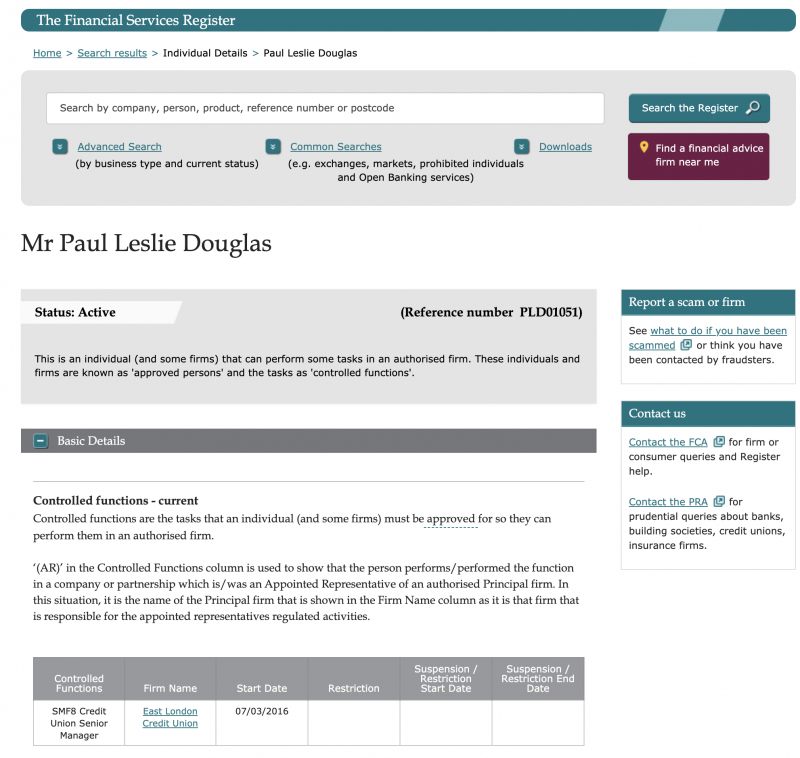

However, if the FCA Financial Services Register is consulted, Mr. Douglas is currently listed as a ’Senior Manager’ of the East London Credit Union, an ‘individual who works for, or used to work for, this firm and is considered an approved person’…

Clearly, there is a significant difference between being ‘a member’ of the East London Credit Union (which most people would take to mean just having an account with the organisation) and being one of a small group exercising control over the East London Credit Union’s corporate affairs.

It is my belief, therefore, that Cllr. Douglas should have declared he was was ‘a senior manager’ and ‘approved person’ of the East London Credit Union on his register of interests form, and his failure to do so is a breach of the Code.

I request that you investigate and respond’.

I attached screenshots of the relevant documents.

Yesterday, Mr Hynes replied:

‘I can confirm that Cllr Douglas was a Director Of ELCU up to January 2017. He has had no connection with ELCU other than holding an account and therefore being a member since that date.

His declaration of interest is correct.

I trust that clarifies the position’.

Today, I checked the Financial Conduct Authority’s Financial Services Register (FSR), and as before it lists Cllr. Douglas as an ‘active’ member of the ECLU board, and a senior manager – see the screenshots below.

Realistically, there seem to be only two ways that My. Hynes’ statement and the information on the FSR can be squared.

{kind=link}

One possibility is that ELCU has kept the Financial Conduct Authority fully informed of personnel changes, but since as long ago as January 2017 the Financial Conduct Authority, for whatever reason, has failed to update the FSR.

The other possibility is that ELCU has not informed the Financial Conduct Authority of personnel changes, apparently unconcerned by the fact that, because of its inaction, information in the public domain about as important a matter as its senior management team, since January 2017 at least, has been highly misleading.

It must be said that neither scenario inspires much confidence.