London Borough of Waltham Forest: the local authority that can’t even finalise its annual accounts (1)

Every year, like other local authorities, LBWF is bound by law to produce its annual accounts, using an external auditor and a timetable specified by the Accounts and Audit Regulations of 2015.

But this year, the procedure has gone wrong, indeed very wrong, and now there is a lively post mortem in progress about who is to blame, and what are the likely consequences.

As regards the 2018-19 audit, LBWF knew the specified time frame well beforehand. Unaudited accounts were due by 31 May 2019, and audited accounts by 31 July 2019, so that the latter then could be signed off by the Audit and Governance Committee.

However, it has recently emerged that LBWF’s auditor, Ernst and Young LLP (hereafter EY), only started work some days after it should have finished; and though, to catch up, it then aimed at a September completion date, as of early December, even the unaudited version of the accounts still remains outstanding.

How has a process that should have been fairly routine and straightforward so spectacularly become derailed?

Some of the factors involved appear to be unfortunate one-offs. A conflict of interest involving a councillor intruded and had to be resolved. In addition, because this was the first year of EY’s contract, and it approached audit differently than its predecessor, KPMG, both sides needed time to familiarise themselves with new expectations and methodologies. And EY, finally, was unexpectedly short of adequately trained staff, especially during the summer months when peak activity was scheduled.

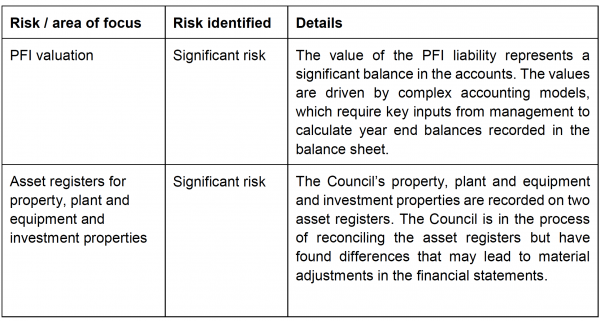

Nevertheless, it is also clear that when EY began examining LBWF’s books it discovered some significant issues, not only with the accounting practices being used, but also, more worryingly, with the basic recording of data. For example, an early EY document summarised ‘additional significant risks in relation to the audit’ thus:

The magnitude of the difficulties is well illustrated by the finding that ‘several schools that had converted to academy status…prior to 2017/18…were still recognised on the Council’s balance sheet’, somewhat awkward for the LBWF staff concerned, to say the least.

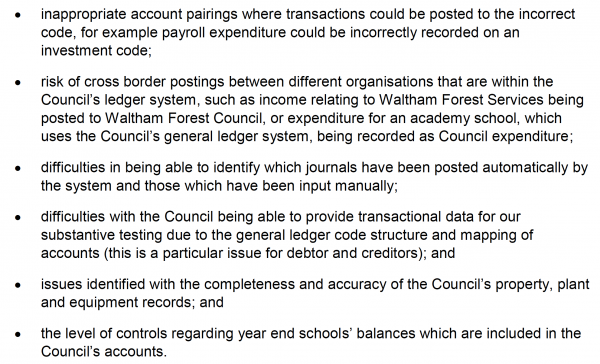

Subsequently, EY has become aware of ‘an increased risk’ that LBWF’s ‘general ledger and accounting records’ also may not be ‘complete or accurate’, with the potential flaws listed as follows:

Inevitably, the bottom line is that EY has ended up having to check much more of the information coming its way than was originally envisaged, and as a consequence the whole process has dragged on.

Unsurprisingly, faced with such an embarrassing delay, both sides are engaged in some finger pointing. Thus, at the Audit and Governance Committee meeting of 26 September 2019, the chair emphasised that the Council ‘needed assurance as to the effectiveness of EY’s approach’ and reportedly added: ‘It is the case that the auditors expressed confidence in the last meeting that the accounts would be signed this evening, but it is more than confidence that is required’.

In response, EY’s representatives have repeatedly stated that they cannot ‘simply…issue an opinion’ confirming the accounts to be ‘true and fair’ until fully satisfied they really are – a sign, perhaps, of their anxiety about being pressured to rush through the niceties.

Meanwhile, there is growing concern about some other aspects of the affair. One is the impact of the delay on the public purse.

In September 2019, it was suggested that the cost of the ‘extra work’ had reached £140,000. It is unclear whether this figure includes both sides’ additional inputs or only one, but there is no doubt that, regardless, the total sum involved subsequently will have increased further, and by some margin.

There is also a question mark over what the current findings mean for past audits. Some of the flaws that EY has discovered go back many years, in fact possibly as far back as 2007. Should previous finalised accounts now be corrected, and if so by whom? Is such correction even possible, given that in the interregnum data is said to have been lost or destroyed? As yet there are no answers, but what’s certain is that, in the end, someone, somewhere, will have to come up with plausible solutions.

Earlier in the year, before all the trouble outlined here, LBWF’s Leader, Cllr. Clare Coghill, drafted an introduction to the annual accounts document which included a notable boast:

‘This year we invited in a peer review team organised by the Local Government Association. The peer team found that the council is “financially well-led” with “ambitious measures in place to take the authority further forward”. As a result, the peer team judged the council to have achieved “a relatively strong financial position compared with other similar local authorities – a position, in fact, that other authorities would envy”’.

So LBWF is ‘financially well-led’, is it?

The biter bit.